Update, 7/31/2018: Check out my new APR to APY calculator!

I am not one who can lecture you on the perils of credit cards from personal experience. I don’t have a redemption arc where I was once buried in credit card and student loan debt, but had an awakening and went on to dig myself out through sheer tenacity. I have 13 credit cards; buy everything using credit cards; got my first credit card at Age 19 (seven years ago); have received tens of thousands of dollars in credit card signing bonuses, cashback, and rewards such as Chase Ultimate Reward points, American Express Membership Reward points, Southwest Airlines Rapid Reward points, and Starwood Hotels Preferred Guest points; have never paid a cent in interest; and pay in full (PIF) every month by the due date (except during the occasional 0.00% APR introductory period).

I have not studied business or finance formally—I went to college for a Bachelor’s in psychology and a Master’s in applied learning and instruction. However, I have been interested in personal finance since I was a teenager in high school and read extensively via Internet searches before receiving my first credit card (a Discover More card, now called Discover It). I heard and internalized the horror stories about penalty interest rates, drowning in debt, bankruptcy, collections, et cetera. I avoided and continue to avoid consumer debt traps, aided by never moving out of my parents’ house, living in Florida where in-state tuition is cheap, having low-income parents which enabled me to receive the maximum Pell grant during my undergraduate studies, and probably a genetic or acquired lack of susceptibility to the lure of over-spending with credit cards.

I started Tippyfi (named after my girlfriend’s orange cat, Tippy—orange cats are always the craziest) to help Americans understand their finances. There are countless financial books, blogs, curricula, and services out there. However, I believe there are ways to financially educate people that haven’t even been discovered yet. Research says that Americans are positively horrible at understanding anything about finance. More research says that it’s getting worse and that taking a financial course (for example, a course in high school or college) doesn’t actually do anything. For some reason in America, finding such a course is like finding a unicorn, and yet the unicorns are all duds.

However, teaching people personal finance in ways that are actually interesting and that matter to them—such as at the point of use (“just in time” before they open a credit card, for example)—does work. Teaching norms or “rules of thumb” also works. For example, Dave Ramsey teaches a rule of thumb that you should never apply for—cancel—cut up—and never use credit cards. This is probably 95% accurate. Based on statistics and credit card issuers’ profit margins, the best advice for the majority of people the majority of the time is to avoid credit cards, just as the best advice is to avoid payday loans, casinos, scratch-off and lottery tickets, multilevel marketing companies, whole-life insurance, and stockbrokers. However, this answer is unsatisfying. It leaves us with a riveting question: WHY?

I always knew that there was a caste system with credit cards. Credit card users are divided into two camps: those who carry a balance from month to month and those who do not. Those who do not carry a balance benefit from the “grace period” each month, paying zero interest, while everyone else is a sucker. I knew that like the tenure track and the adjunct track in academia, those on the grace-period track are successful, while those on the interest-paying track get screwed over.

However, not having first-hand knowledge of the interest-paying track (i.e., carrying a balance from month to month), I did not realize how rotten it is. I had read many articles like this one from Money Under 30 that talks about “residual interest” being something that “accumulates between the billing statement date and the date you pay the bill.” In passing, I had heard of credit card issuers that actually charge suckers interest on their purchases from the date of the purchase instead of the date the monthly billing cycle ends. However, I assumed these were garbage, sub-prime cards from bandits such as First Premier Bank.

While figuring out how to write an article about credit cards for Tippyfi, I dug into the terms for the Chase Freedom Visa card (preserved in their present state here). The Chase Freedom card is known as one of the “good” ones that those who are rebuilding their credit aspire to obtain. Chase’s market share is massive—way ahead of Bank of America and second only to American Express. What I found in their terms shocked me.

Page 7: Your account is in an interest-free period when you pay your New Balance as shown on your statement every month by the due date and time. During this period, you will not pay interest on purchases. [This is the grace-period track for those who pay in full each and every month.]

Page 7: We charge interest on purchases from the date the transactions appear on your account (until the balance is paid in full) when your account is not in an interest-free period. [Emphasis mine. This applies to EVERYONE who carries a balance from month-to-month.]

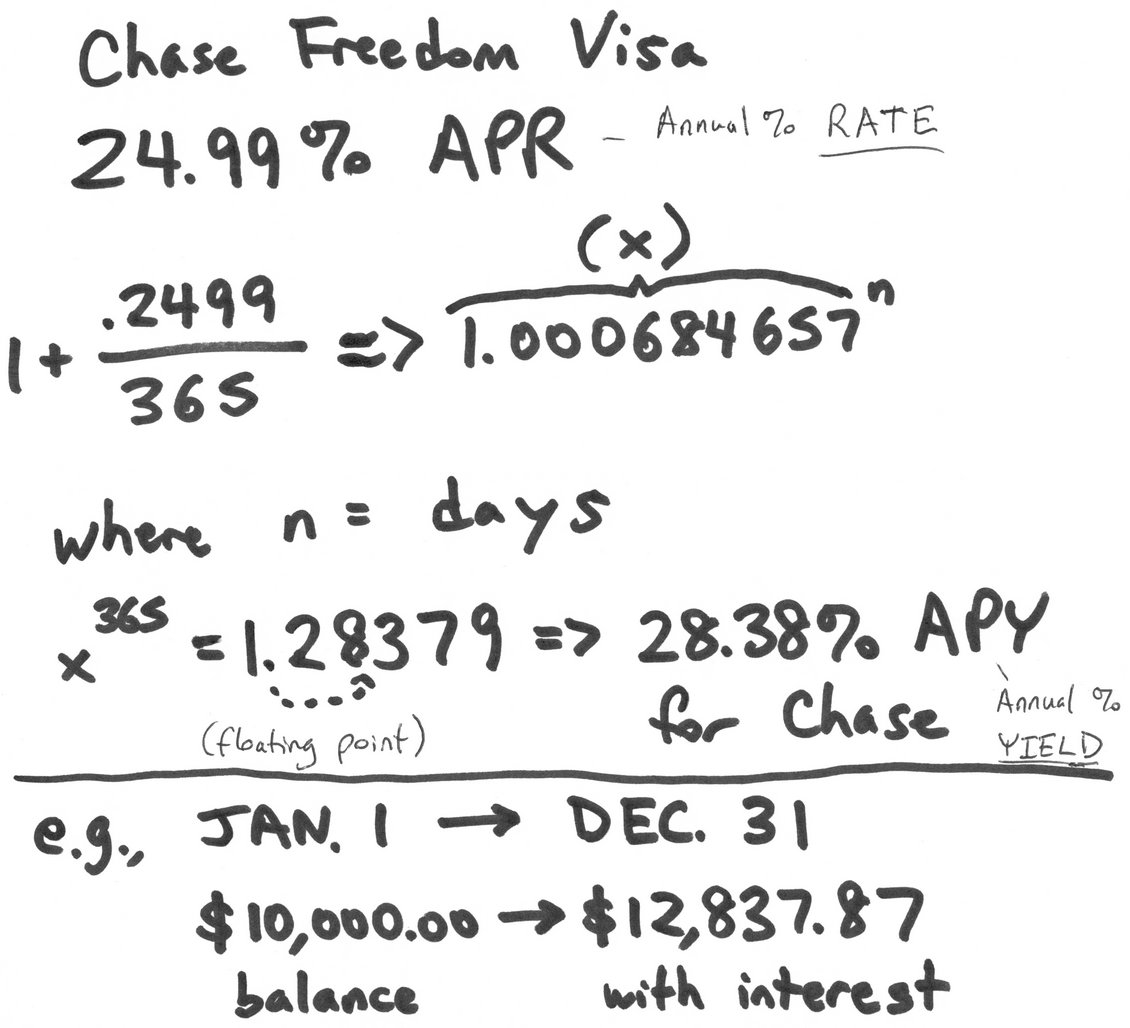

Page 13: We calculate a daily balance for each type of transaction and use the daily balances to determine your interest charges. … We take the beginning balance for each day and add any interest charge from the prior day (known as compounding of interest). … To get the daily interest rate for each type of transaction we divide the APR by 365. [Emphasis mine. I guess it should have been obvious that they compound interest every day, but this was not something I gave much thought to before.]

Like in my prior article on investing, at this point I locked myself in a room with a Sharpie, a few sheets of copy paper, and, this time, a scientific calculator.

Chase claims their annual percentage rate (APR) for the Chase Freedom Visa ranges from 15.24% to 24.99% based on credit worthiness. We know many Chase Freedom recipients are fairly new to credit cards, and many more who aren’t probably wind up with the 24.99% APR too. What we see above is, in part, the difference between annual percentage rate (APR) and annual percentage yield (APY). At first glance you might think a balance of $10,000.00 would increase to $12,499.00. However, they compound the interest daily. This means the APY isn’t 24.99%. It’s the daily compounding coefficient to the 365th power. This means the APY is actually 28.38%, not 24.99%. A balance of $10,000.00 on January 1, assuming a constant level of indebtedness, becomes $12,837.87 at year’s end.

Update, 7/31/2018: Check out my new APR to APY calculator!

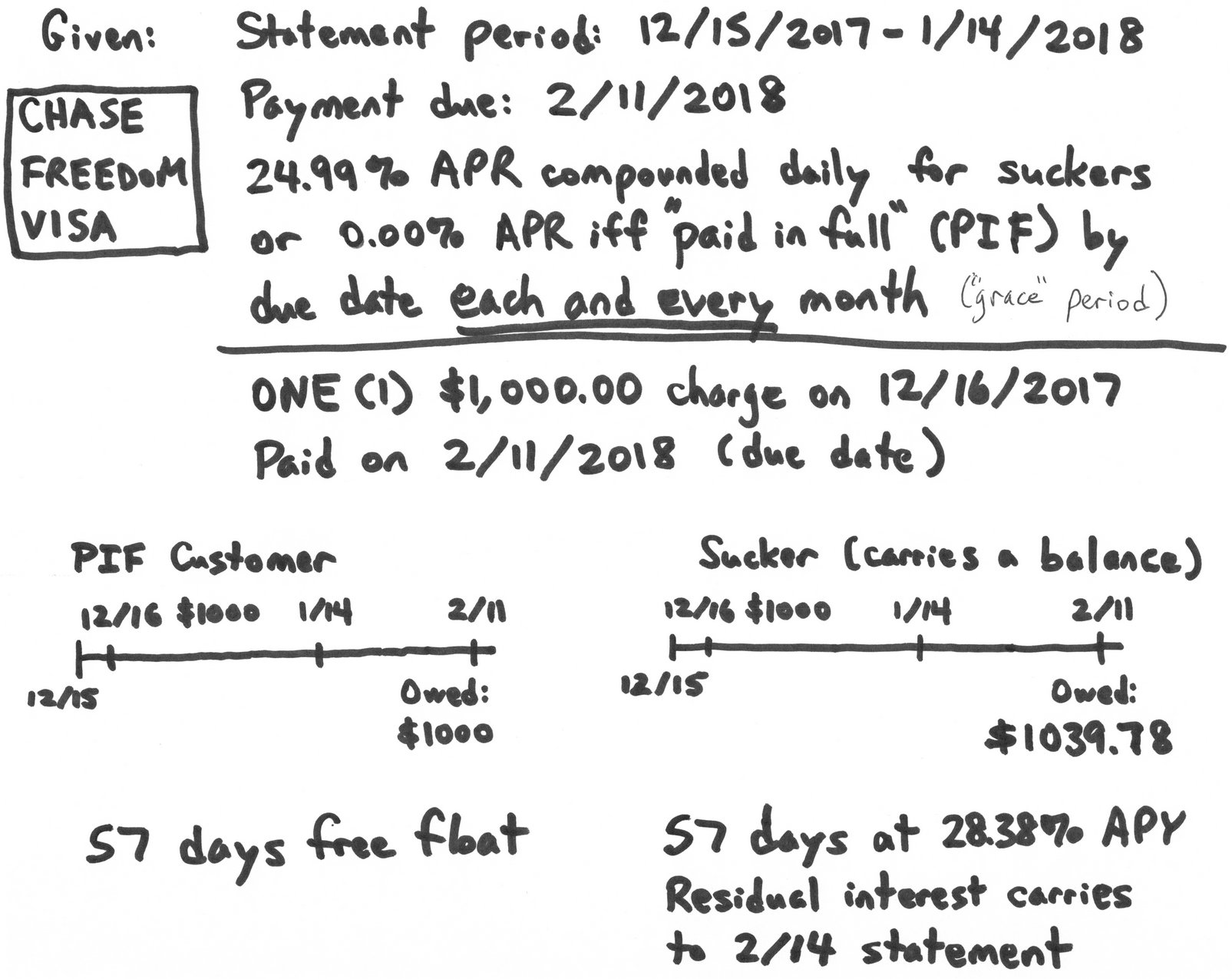

Next, I submit to you a concrete example of a grace-period track, paid-in-full (PIF) customer vs. a “sucker” who is on the interest-paying track. Both customers’ statements cut on 1/14/2018 with a payment due date of 2/11/2018. Both customers charge $1,000.00 to their Chase Freedom Visa on 12/16/2017 and pay the statement balance on 2/11/2018.

In this example, the PIF customer actually gets 57 days free float. They enjoy the privilege of borrowing $1,000.00 from Chase for 57 days without paying interest. However, all other customers who suffer a 28.38% interest rate pay $39.78 for this privilege.

BUT WAIT—IT GETS WORSE

Those who on the sucker’s track—the interest-paying track—don’t have an obvious way to get off it due to a catch called “residual” or trailing interest. My Sharpie drawing falls a bit short here, but, going back to the Money Under 30 article, the sucker actually gets a bill for $1,000.00 plus 29 days interest, but additional interest accumulates between the statement date and the date they pay their statement balance. In this example, the sucker gets a bill for $1,020.05 on 1/14/2018 and pays it on 2/11/2018 (in full!—for a change), but by 2/11/2018, the true amount owed is actually $1,039.78, because it includes interest for the additional 28 days between the statement date and the date paid that would have constituted the grace period for the customer who pays in full each and every month. This is why I wrote the mathematical word iff above, which means “if and only if.”

The sucker thinks she or he has made a change, earning her or his way back to the promised land of the tenure-grace-period track. However, due to the existence of $19.73 of residual interest that was not and could not be paid, purchases on the next statement continue to immediately begin accruing finance charges. There is actually, quite literally, no obvious way for someone to get back on the grace-period track. In fact, Chase presents this error message to customers suckers who attempt to pay more than their statement balance to cover residual interest and get back on the grace-period track:

Although it is rude for me to call them suckers because interest-paying customers are the majority of American credit card users, you can bet this is what the credit card issuers think of you. Don’t be a sucker. Stay with me, and I’ll tell you how.

Firstly, the Money Under 30 article says you can try “contacting the credit card issuer and request[ing] the full payoff amount as of the date that you plan to actually make the payoff payment.” I doubt this would work. They would probably explain that they have no way to process such a payment. It’s funny how things that can’t be done are always the things that would benefit the customer.

Secondly, it might seem you could make no additional charges on the next statement. Then, the following statement would contain only the residual interest from the prior statement. However, even then, more residual interest might continue to accrue on the residual interest from the prior statement and haunt you on the following statement. Not having firsthand experience, I wouldn’t know.

Thirdly, the real solution: You need to do a bill payment or other ACH push payment from an outside financial institution to over-pay your Chase Freedom Visa balance. You can’t do this from within Chase’s world. You could do a bill payment at Walmart, or push money out from your checking account at virtually any other bank using their bill payment feature. Pay more than enough, as having a negative (credit) balance on a credit card is no problem—the balance simply acts as a credit toward future purchases on the card. This is the way to stop being a sucker and get back on the grace-period track in a single billing cycle.

I would hazard a guess that more than 95% of Americans are oblivious to the grace-period track vs. carrying a balance, residual interest, and the trickery employed by Chase and other credit-card issuers to keep you off the grace-period track. This trickery is intensely profitable and attractive. Even Starbucks, the beloved American coffee chain from Puget Sound who graces their employees—even part-timers—with free college, inexpensive health insurance, a 401(k) match, and shares of Starbucks stock, has fallen. Last week (on 2/01/2018), they announced the introduction of the Starbucks credit card, issued by—wait for it—Chase. I kid you not. With an unnecessary and ridiculous $49 annual fee, to boot. Even the Chase Freedom card has no annual fee.

Don’t get the Starbucks credit card. Don’t ever carry a balance on a credit card. Don’t be a sucker.

The mission of Tippyfi is to revolutionize financial education so that the majority of Americans stop being suckers. For writing an article that is simultaneously an attack on academia’s tenure caste system, an attack on JPMorgan Chase & Co., and an attack on our beloved Starbucks, I am off to a rollicking start.

Wow – will I make myself look dumb if I admit that I NEVER would have thought of the solution you gave? Everybody who has a credit card or is thinking of getting one should read this!!

Thanks, Joanie! I would bet 95% of people wouldn’t think of pushing a bill payment from an outside bank to over-pay the credit card to wipe out residual interest in one statement. For people who are carrying a balance, if they continue to use credit cards, the best thing is to do all their purchases on a separate credit card that they keep on the grace-period track. That way, their purchases on the second card don’t get subjected to interest at all. If they continue buying with the card they carry a balance on, 28.38% APY of interest starts accruing from the date of each purchase with no grace period (if their APR is 24.99% compounded daily).