Today, February 5, 2018 we saw a large decline of the Dow Jones Industrial Average and other stock market indices.

Although the stock market has had phenomenal gains since 2009, and especially in the past year, we are seeing a temporary decline that, in the past week, has erased the past two months of market gains.

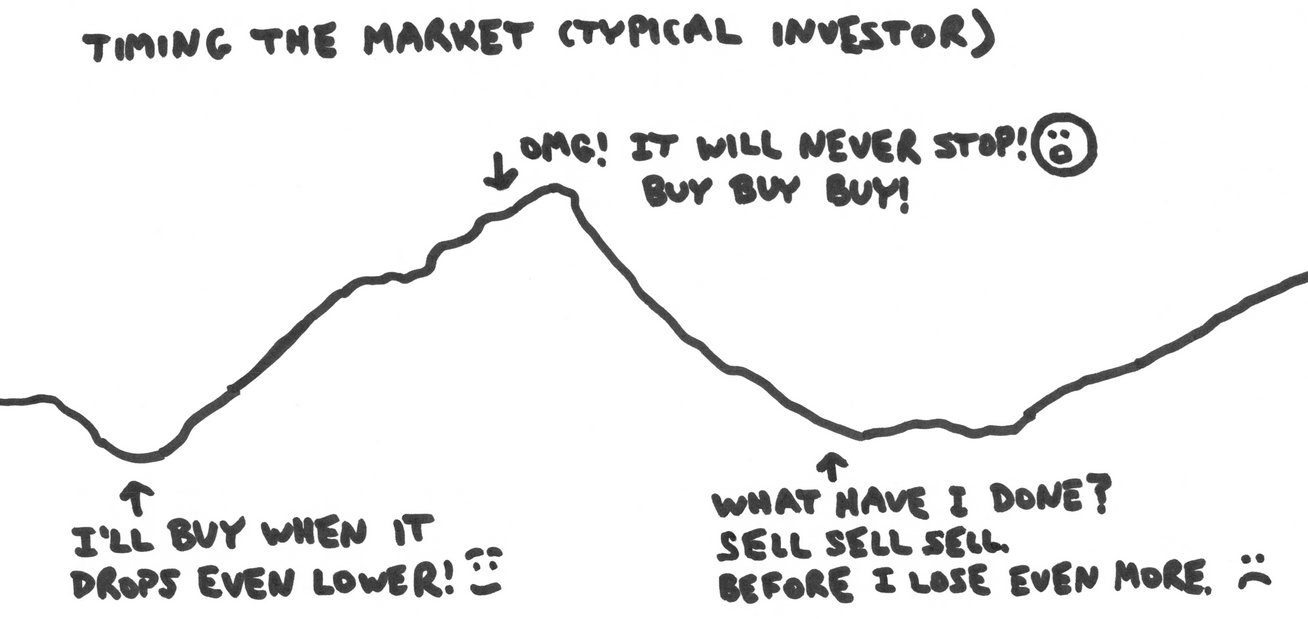

Having a bias toward action is helpful in many areas of life, but investing is one area where inaction wins. In fact, investors who have died or simply have forgotten about their investments have results superior to the typical investor. The typical investor buys high, sells low, and then has fear of missing out (FOMO) and buys back in when the market is high again. The present “crash” spurs typical investors to sell, supposedly to prevent further losses. The typical investor’s behavior looks something like this:

In the market, buying activity is high when prices are high, and selling activity is high when prices are low. Therefore, although the S&P 500 gained about 10% per year over 20 recent years (1996–2015), the average investor only gained about 5% per year.

Trying to time buying into the market at market dips (“buy low”) looks like this, if you’re lucky:

However, the more typical investor probably goes through a cycle like this:

This is a very painful emotional process involving much sadness, regret, and inward anger for things like not “seeing the signs” earlier. After an investor does this a few times, they might end up just putting their money in a certificate of deposit rather than avoiding the pain of the stock market. Then, they permanently miss out on capital gains, which were about 10% per year on average during 1996–2015. This ends up costing them dearly in the long run.

On the other hand, the atypical investor uses a “buy and hold” strategy that looks something like this:

The atypical investor doesn’t sell when the market goes down nor when it goes up. In fact, following the financial news at all is hazardous for your financial health. Investing in any individual stock or sector is also hazardous for your health, which is one reason why “passive” index funds of the entire market are preferable. Another reason is that their management fees are very low—for instance, 0.04% per year as compared with 0.50–2.00% per year for more complex, “sophisticated” funds. Funds that are actively managed by a stockbroker based on “market signals” and “timing” fail to out-perform the market, while costing you a bundle each year (e.g., at 1%, $1000 on $100,000 each year compared to $40 with a Vanguard fund). Of course, it can be hard to figure this out via Google when so many of the articles are from broker–dealers like Morgan Stanley who want to sell you their services.

Therefore, the foremost principles for the atypical investor are to (a) passively invest a majority of one’s portfolio in low-fee indices of the broader stock market (e.g., S&P 500, whole U.S. market, or even whole global market) and (b) invest for the long haul and avoid behavioral traps such as trying to time the market or getting stressed over temporary market declines. A third principle is (c) avoid taxes through IRAs, 401(k)s or 403(b)s, and other lawful mechanisms, but even following the first two principles alone puts you far ahead of most investors.

The ideas presented here should not be taken as financial or legal advice. The drawings in this post are all by Richard Thripp, inspired by Carl Richards’ Sharpie-on-napkin drawings. Many of the ideas here are borrowed from Richards’ book; the Bogleheads forum named after Vanguard’s founder, Jack Bogle; and the Maven Money podcast by Andy Hart, a British financial adviser.

Five pingbacks